As instant payment networks expand globally, financial institutions must implement advanced monitoring systems capable of identifying fraud, sanctions risks and money laundering within seconds. This shift is driven by regulatory changes, technological innovation and the rapid adoption of instant payment rails worldwide.

The rise of real-time AML monitoring in instant payment systems

Instant payment systems are transforming global financial infrastructure. Traditionally, payments could take hours or even days to settle. Today, however, modern payment rails enable transfers within seconds, 24 hours a day, seven days a week.

Examples include SEPA Instant in the European Union, Faster Payments in the United Kingdom, UPI in India and FedNow in the United States. While these systems significantly improve customer experience and business efficiency, they also introduce new financial crime risks. Because transactions settle almost immediately and are typically irreversible, financial institutions no longer have the luxury of reviewing transactions after settlement.

Consequently, institutions must identify suspicious activity before or during the payment process.

This operational reality has accelerated the adoption of real-time AML monitoring frameworks, supported by artificial intelligence, advanced analytics and automated compliance systems.

Global instant payment systems and their 2026 compliance requirements

Instant payment infrastructures now operate across multiple jurisdictions, each with its own regulatory expectations and compliance frameworks.

| System | Region | 2026 Compliance Focus |

|---|---|---|

| FedNow | United States | Adherence to FinCEN SAR obligations and FedNow fraud risk management guidance, including use of tools such as the FraudClassifier Service and the Request for Return of Funds (RROF) process for suspected fraudulent transactions. |

| SEPA Instant | European Union | 10-second payment execution under the EU Instant Payments Regulation and customer-level sanctions screening against EU consolidated lists at least once every 24 hours. |

| Faster Payments | United Kingdom | APP fraud reimbursement rules governed by the Payment Systems Regulator (PSR) and the UK government’s National Payments Vision strategic framework |

| UPI | India | Compliance with RBI KYC Master Directions and PMLA obligations for participating banks and payment service providers, alongside real-time fraud monitoring for instant transactions. |

As instant payment adoption increases, financial institutions must ensure their compliance infrastructure can operate at the same speed as their payment systems.

The EU instant payments regulation and the 10-second rule

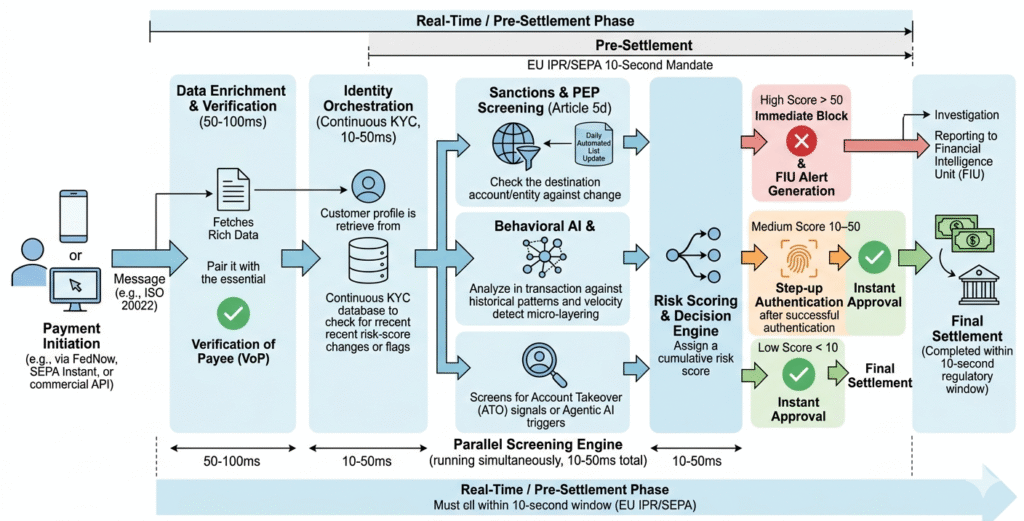

The European Union’s Instant Payments Regulation (IPR) represents one of the most significant regulatory developments in modern payment systems. Under this regulation, payment service providers participating in SEPA Instant must ensure that transferred funds are available to the recipient within 10 seconds. This strict settlement requirement dramatically reduces the time available for traditional compliance checks. As a result, financial institutions must rely on automated monitoring systems capable of evaluating risk within milliseconds.

Sanctions screening requirements under article 5d

Another major change introduced by the EU Instant Payments Regulation concerns sanctions screening obligations. Historically, financial institutions screened every payment transaction against sanctions lists. However, performing sanctions checks for each instant payment could slow down processing and undermine the speed of instant payment networks. Under Article 5d of the Instant Payments Regulation, payment service providers offering instant payments must screen their customer base against EU consolidated sanctions lists at least once every 24 hours. This approach ensures that institutions maintain sanctions compliance while preserving the operational efficiency of instant payment systems.

It is important to note that point-of-onboarding sanctions screening for new customers remains a separate, ongoing obligation. The daily screening model applies to the monitoring of existing customer portfolios. For many institutions, implementing these controls requires robust compliance infrastructure and expert guidance through Sanctions Screening Consulting and AML compliance advisory services.

Verification of Payee (VOP): a critical fraud prevention mechanism

Another important regulatory development in instant payments is the introduction of Verification of Payee (VoP) systems. VoP confirms that the name entered by a payer matches the actual account holder of the receiving account. This measure is designed primarily to reduce Authorized Push Payment (APP) fraud, one of the fastest-growing forms of financial crime.

In the United Kingdom, APP fraud reimbursement rules introduced by the Payment Systems Regulator (PSR) require mandatory reimbursement for eligible victims of fraud occurring through the Faster Payments system. Reimbursement is capped at £85,000 per claim, with costs shared between sending and receiving payment service providers.

ISO 20022 is becoming the global standard for payment messaging

Another major milestone shaping the future of AML monitoring is the global migration to ISO 20022 payment messaging standards. SWIFT began migrating cross-border payment messaging to the ISO 20022 standard in March 2023. During the transition period, financial institutions support both legacy MT and ISO 20022 (MX) messages. The coexistence phase for CBPR+ payment messages ends in November 2025, after which cross-border payments on the SWIFT network must use ISO 20022 messaging formats. ISO 20022 provides significantly richer transaction data, including structured information about the sender, recipient and payment purpose. This richer data environment greatly improves the effectiveness of transaction monitoring systems.

Within SWIFT’s cross-border payment messaging network, November 2026 marks the deadline after which payment messages must use fully structured address fields. Financial institutions must therefore ensure that payment messages contain structured address data. Structured payment information improves the accuracy of sanctions screening, transaction monitoring and financial crime detection.

How criminals exploit instant payment systems?

Financial criminals adapt quickly to technological changes in the financial sector. One of the most prominent techniques used in instant payment environments is micro-layering. Micro-layering refers to the rapid dispersal of small amounts of money across thousands of accounts within seconds. Because each individual transaction may appear low risk, detecting the broader pattern requires advanced monitoring technology.

An emerging area of discussion involves so-called “agentic AI payments” — transactions initiated autonomously by AI systems rather than human actors. Regulators and financial crime experts have begun exploring how such technologies could introduce new fraud and money laundering risks in automated financial ecosystems.

These evolving threats highlight the need for financial institutions to implement advanced analytics and behavioral monitoring tools capable of detecting complex transaction patterns.

Why is real-time AML monitoring now essential?

Real-time AML monitoring systems analyze payment transactions the moment they are initiated.

When a transaction request is submitted, the monitoring system evaluates multiple risk indicators simultaneously. These indicators typically include:

- Customer risk profile

- Historical transaction patterns

- Geographic risk exposure

- Transaction velocity

- Network relationships between accounts

If the system identifies unusual or suspicious activity, the transaction can be delayed or blocked before settlement occurs. This capability is critical in instant payment environments where transactions may otherwise complete within seconds.

The role of artificial intelligence in AML monitoring

Artificial intelligence is increasingly used to enhance financial crime detection. Machine learning algorithms can analyze massive volumes of transaction data and identify suspicious patterns that traditional rule-based monitoring systems may overlook.

Graph analytics can uncover relationships between accounts, helping investigators detect organized money laundering networks.

In addition, AI-driven monitoring systems significantly reduce false positives by prioritizing high-risk alerts. This allows compliance teams to focus their investigative resources more efficiently.

Disclaimer

This article is for informational purposes only and does not constitute legal or regulatory advice. Organizations should consult professional advisors or contact Compliance7 for jurisdiction-specific AML compliance guidance.