Anti-Money Laundering (AML) compliance has evolved into one of the most expensive and operationally demanding obligations for regulated organizations worldwide. What was once a targeted regulatory safeguard has grown into a complex ecosystem of controls, systems, staffing models and reporting requirements that now command substantial budgets and sustained executive attention. Across banks, fintechs, payment institutions, virtual asset service providers and designated non-financial businesses, AML costs continue to rise year after year. Global estimates place annual spending on AML, KYC, sanctions screening and financial crime compliance in the hundreds of billions of dollars, yet financial crime itself shows no signs of retreating. This growing disconnect between compliance expenditure and measurable impact has triggered an overdue question: Is AML compliance delivering outcomes proportionate to its cost?

It is within this context that the Financial Crimes Enforcement Network (FinCEN) issued its Formal Notice of Survey on AML/CFT Program Costs, inviting industry participants to quantify the true cost of compliance. This move reflects a notable shift in regulatory thinking – from assessing whether institutions are complying, to examining whether the compliance framework itself is efficient, proportionate and effective.

This article explores what FinCEN’s survey tells about the rising burden of AML compliance, the structural reasons costs continue to escalate and how organizations can rebalance their programs toward effectiveness without increasing regulatory risk.

What Do We Mean by “AML Cost vs. Effectiveness”?

AML Compliance Cost refers to the total financial, operational and human resources required to design, implement, maintain and defend an AML/CFT program. This includes staffing, technology, audits, remediation efforts, regulatory engagement and ongoing governance.

AML Effectiveness refers to how well an AML program actually identifies, mitigates and disrupts illicit financial activity while producing useful intelligence for regulators and law enforcement, rather than simply generating compliance outputs.

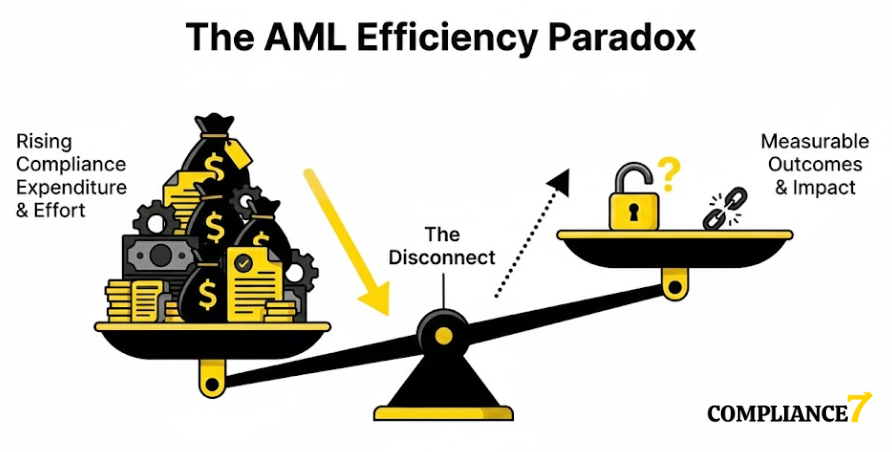

The AML Cost vs. Effectiveness Paradox emerges when AML spending continues to increase, yet outcomes-such as actionable Suspicious Activity Reports (SARs), reduced exposure to financial crime or improved supervisory confidence fail to improve at the same pace.

This paradox sits at the core of FinCEN’s survey.

Why FinCEN Is Re-Examining the Cost of AML Compliance

FinCEN’s focus on AML costs is directly connected to the AML Act of 2020, enacted by the U.S. Congress as part of a broader effort to modernize the AML/CFT regime. The Act explicitly emphasizes that AML programs should be assessed based on their usefulness to law enforcement and national security, not merely on procedural completeness.

For years, AML supervision globally has leaned heavily on inputs: policies documented, alerts generated, SARs filed and controls evidenced. Over time, this input-driven model encouraged institutions to equate higher volumes of activity with stronger compliance. As a result, many organizations expanded controls defensively – lowering thresholds, increasing alert volumes and filing SARs primarily to demonstrate regulatory diligence.

By issuing a Formal Notice of Survey on AML/CFT Program Costs, FinCEN is signaling that this model may no longer be sustainable. The survey implicitly acknowledges that compliance burden itself can undermine effectiveness by diverting resources away from genuine risk areas and overwhelming both institutions and authorities with low-value information.

The True Cost of AML Compliance: Beyond Technology Spend

AML compliance costs are often discussed through the lens of technology investment, but this view captures only a part of the picture. In practice, AML costs are layered, compounding and deeply operational.

The most significant cost driver remains human capital. Despite advancements in automation, AML programs still rely heavily on manual judgment. Analysts review alerts, investigate transactions, perform enhanced due diligence, draft SARs and respond to regulatory queries. As regulatory expectations rise, demand for experienced compliance professionals increases, driving up salaries, turnover and training costs. For many institutions, staffing represents more than half of total AML expenditure.

Technology costs add another layer of complexity. Many organizations operate fragmented compliance stacks-separate systems for transaction monitoring, sanctions screening, KYC onboarding and case management. Poor integration between these systems creates data silos, duplicate alerts and reconciliation challenges that increase operational effort rather than reducing it.

A further hidden cost lies in false positives. Rules-based monitoring systems generate large volumes of low-risk alerts that still require investigation and documentation. This inflates workloads, drives headcount growth and reduces the time available to focus on genuinely suspicious activity.

Finally, regulatory examinations and remediation programs introduce substantial indirect costs. Independent audits, regulatory lookbacks, consultant engagements and multi-year remediation efforts can lock institutions into elevated compliance spend long after the original issue arose.

Structural Drivers Behind Rising AML Compliance Costs

To understand why AML costs continue to escalate, it is essential to look at the structural forces shaping compliance programs today.

At a high level, three structural drivers dominate AML cost growth:

- Human Capital Dependency

- Technological Fragmentation

- Defensive Over-Compliance

Human capital dependency reflects the ongoing reliance on manual investigation and expert judgment. AML remains difficult to scale efficiently, making costs structurally inflationary.

Technological fragmentation arises from disconnected systems and poor data integration. Instead of enabling efficiency, fragmented technology stacks often multiply alerts and increase manual intervention.

Defensive over-compliance is driven by fear of enforcement actions. Institutions respond by filing low-value SARs, lowering thresholds and applying blanket controls, which increases cost while diluting effectiveness.

Together, these drivers create a self-reinforcing cycle of higher spend, greater complexity and stagnant outcomes.

Burden vs. Effectiveness: Why More Compliance Activity Does Not Mean Better Results

The tension between burden and effectiveness is most visible in Suspicious Activity Reporting. While SAR volumes have risen consistently, multiple studies and public statements from law enforcement agencies and international bodies have noted that only a small proportion of reports lead to actionable investigations.

This creates a system where compliance success is measured by how much is produced, not by how useful that output is. Institutions file defensively to protect themselves, while regulators and law enforcement struggle with information overload.

FinCEN’s survey reflects growing recognition of this imbalance and raises a fundamental question: Should AML programs be evaluated by activity levels or by their contribution to actual risk reduction?

Key Metrics to Shift Focus: From Volume to Value

A meaningful shift toward effectiveness requires redefining how AML performance is measured. Traditional metrics focus on activity, while emerging expectations emphasize impact.

Volume vs. Value: AML Metrics Comparison

| Metric Type | Volume-Driven (Old Focus) | Value-Driven (New Focus) |

| Primary Goal | Demonstrate compliance activity | Demonstrate impact and risk reduction |

| Core Measure | SAR volume, alert counts | SAR usefulness (law enforcement feedback) |

| Efficiency Lens | Size of compliance team | False positive reduction rate |

| Regulatory Outcome | Procedural compliance | Faster remediation, supervisory confidence |

FinCEN’s cost survey strongly suggests that future supervisory frameworks will increasingly favor value-based indicators over sheer volume.

Who Bears the AML Cost Burden Most Heavily?

The impact of rising AML costs is not evenly distributed. Smaller institutions and fintechs often face disproportionate pressure, as fixed compliance costs consume a larger share of revenue. This can constrain growth, delay market entry and contribute to de-risking practices.

Digital-first and cross-border businesses face additional challenges. Rapid scaling and evolving product offerings strain AML frameworks that were not designed for speed or flexibility, often leading to costly retrofits after licensing.

Large multinational organizations struggle with inconsistent regulatory expectations across jurisdictions, limiting economies of scale and further inflating global compliance budgets.

How Organizations Can Rebalance AML Cost and Effectiveness?

Organizations that successfully control AML costs do not weaken controls; they refine them. Strong risk assessments allow resources to be focused where exposure is highest. Improved data quality often delivers greater efficiency gains than additional technology. Most importantly, redefining success metrics aligns internal incentives with regulatory outcomes.

This shift-from defensive, volume-driven compliance to proportionate, outcome-driven AML – is precisely what FinCEN’s survey appears to encourage.

Key Takeaways for Decision Makers

The rising cost of AML compliance is not simply a budgeting concern – it is a structural challenge that affects resilience, growth and regulatory trust. FinCEN’s AML compliance cost survey signals a decisive shift toward evaluating programs based on effectiveness, proportionality and outcomes. Organizations that adapt now will be better positioned to manage costs, meet future regulatory expectations and deliver genuine financial crime risk reduction.

Disclaimer

This article is for informational purposes only and does not constitute legal or regulatory advice. Organizations should consult Compliance7 or qualified professionals for jurisdiction-specific AML, KYC and regulatory compliance guidance.

The disconnect between the rising costs of AML compliance and the effectiveness in reducing financial crime is concerning. It’s interesting to see that FinCEN is taking a more data-driven approach with their survey, focusing not just on whether institutions comply, but whether the compliance efforts are actually making a tangible difference.